Why a comparative view matters

Consumers used to long lines and paper forms now expect speed and clarity. A comparative look shows how fintech platforms reduce friction compared with legacy banks, especially for revolving credit products. For travelers, gig workers, and small owners in urban centers like Mexico City, the practical difference is tangible: faster underwriting, clearer APR displays, and often a digital wallet for convenient repayments. I’ll reference didi finanzas early because it represents this shift from branch-first systems to app-first credit lines.

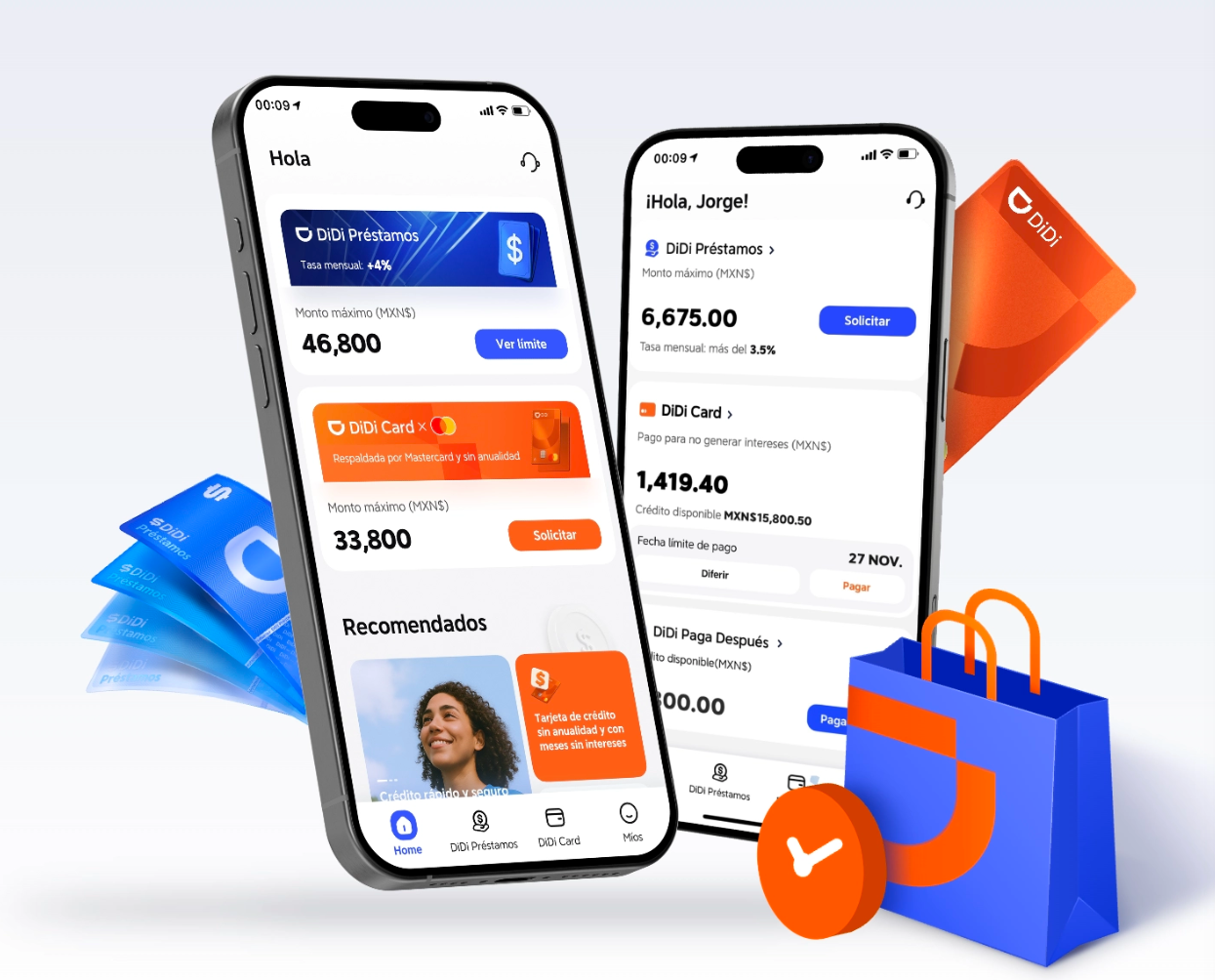

How modern providers differ from banks on revolving credit

Traditional banks still rely on office visits, manual document checks, and legacy back-end systems. Modern providers automate underwriting and use real-time scoring to open a credit line in hours instead of weeks. That changes daily cash flow for someone who needs a flexible balance rather than a fixed loan. Trust is critical here — consumers ask if the platform is legitimate. For reassurance, look for transparent fee tables and regulatory disclosures; resources like didi finanzas es confiable can help verify credibility in markets where fintechs are new.

Practical steps to use revolving credit well

Adopt a few simple habits when you move from a bank to a fintech service. First, review the APR and any maintenance fees before accepting a credit line. Second, set alerts in the app to avoid late payments. Third, keep an emergency buffer — a revolving credit line is best as a backup, not your primary savings. These actions reduce interest costs and protect your credit score in the long run.

Common mistakes people make — and how to avoid them

Users often treat revolving credit like free money and carry high balances month to month. That increases interest and damages credit utilization ratios. Another mistake is not reading the fine print on fees for early payoff or card replacement — small costs add up. A useful habit is periodic reconciliation: match monthly statements to app transactions and flag anything unfamiliar. Also, keep your KYC details current to prevent sudden freezes — it’s administrative, but it saves headaches later. — Remember, simple maintenance avoids surprises.

Alternatives worth considering

Not every user should switch. Credit unions and community banks can offer lower APRs for certain profiles, and secured lines through existing banks might be better for rebuilding credit. Peer-to-peer lenders and buy-now-pay-later services are distinct alternatives depending on purpose: short purchases versus ongoing working capital. Compare these options on three dimensions: cost (APR and fees), access (time to approval), and control (repayment flexibility).

Checklist before you commit

Use this short checklist to compare options directly:- Confirm the effective APR and any compounding methods.- Check customer support hours and dispute procedures.- Verify data protection policies and where your data is stored.These points clarify trade-offs and reduce regret after signing.

Closing guidance

Three golden rules to evaluate any revolving credit product: 1) prioritize transparent pricing over initial convenience; 2) measure true cost by simulating realistic balances for three months; 3) ensure customer support is reachable in your time zone. Follow these and you’ll choose a solution that truly fits your cash flow needs. Final note — many users find the transition from banks to platforms smoother than expected because the apps handle routine tasks automatically and show balances clearly. DiDi Finanzas. — thoughtful.