User-first opening: the reality for many without score

Many people start work without a credit score — gig drivers, new graduates, recent migrants — and they need money to fix a car, buy tools, or cover rent. For those folks, platforms like didi prestamos have become practical entry points into lending. This piece looks at how DiDi Finanzas approaches users with no credit history, using a plain, actionable voice so you can decide fast and clearly.

What DiDi Finanzas actually does for beginners

DiDi Finanzas tends to focus on income-based signals rather than long-standing credit files. That means alternative underwriting — looking at recent earnings, ride history, or app activity — rather than a traditional credit score. The app often shortens KYC steps and offers quick approval windows, so loan term and principal are presented up front. For people in Mexico City and other major urban areas, this model matched real need during the COVID-19 pandemic when many lost regular banking relationships and needed quick cash.

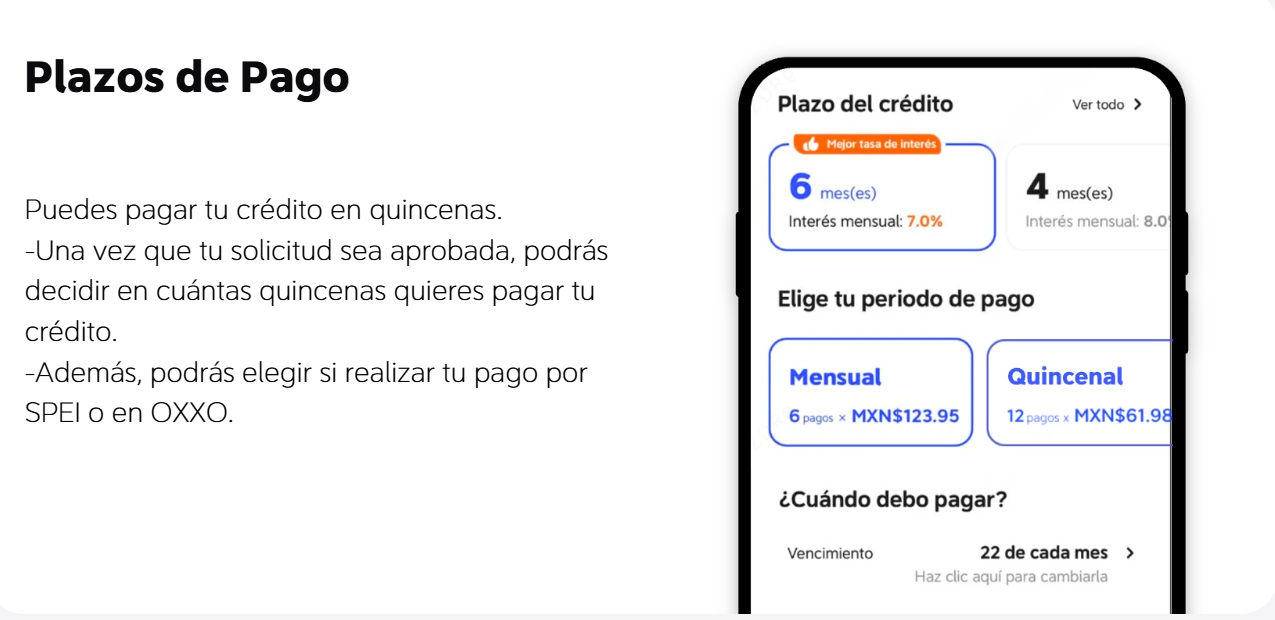

Step-by-step: how to start with little or no credit

Start simple. Link your earnings statement inside the app. Provide ID, comply with KYC, and accept the APR and repayment schedule you can meet. Expect a short approval cycle if your income flow is clear. Keep documentation handy: bank deposits, ride logs, or pay stubs work best. Use the first small loan to build a consistent repayment record — that becomes your new data trail. Over time, timely payments improve your candidacy for larger offers.

Common mistakes new users make — and how to avoid them

People new to online lending often bite off too much. They accept the maximum principal without checking monthly cash flow. They ignore fees and focus only on the headline rate. They miss the loan term alignment with their income schedule. — Pause, and run the numbers. Small loans with consistent, on-time repayments create a positive credit pattern; bouncing a payment creates trouble faster than one thinks.

Comparing options: when DiDi fits, and when to look elsewhere

DiDi Finanzas is useful for short-term, income-backed needs and for users who value speed and simplicity. Alternatives include neobanks with small-credit products, credit unions with starter loans, or peer-to-peer lending marketplaces that may offer lower APR but require more documentation or collateral. If you need long-term credit—mortgage or business capital—traditional lenders or secured loans might be wiser. For instant needs, however, platforms advertising prestamos en linea al instante can be the most practical route for quick liquidity.

Practical signals of trust: what to watch in a lender

Look for clear disclosure of APR, a readable repayment schedule, and an accessible support channel. Check whether the platform reports repayments to credit bureaus; that’s how your new history gets recorded. Also watch for prepayment or late fees and any automated debits that could catch you off-guard. These are plain user-safety checkpoints — no jargon, just safeguards.

Golden rules for choosing the right path (three metrics)

1) Cash-flow fit: Choose loans where monthly payments are ≤30–35% of your predictable take-home pay. That prevents stress on daily expenses.

2) Transparency score: Favor lenders that show APR, total cost, and exact repayment dates before you sign. If you don’t see it, walk away.

3) Reporting and build: Prefer services that report positive payments to bureaus or link to longer-term credit-building tools; this turns short loans into future leverage.

These measures give you practical control, and they point to when DiDi Finanzas makes sense — especially for quick, income-backed help. DiDi Finanzas fits as a bridge: it converts daily earnings into credit access while you build a repayment record for larger products later. — small steps, steady change.